Almond prices on the tear

In recent weeks as the Californian harvests has commenced almond prices have been rallying, as the 3.0bnlb USDA forecast may be considered optimistic. Key points:

Almond prices: USD almond prices have rallied ~26% from the bottom, with the Stratmarkets Almond index now at ~US$3.11/lb and at a higher level than that just prior to the Jul’25 Objective estimate. The move is on the back of mixed early harvest reports in California, calling into question the 3.0Bnlb USDA forecast. In AUD terms, almond prices have moved to ~A$10.35/kg, a 3-month high and up +19% YOY.

Input costs: Major cost inputs in water and fertiliser are broadly unchanged from our previous update. Our baseline assumptions are for +6% YOY growth in costs per kg (on a 29kt equivalent basis).

Weather outlook: The three-month outlook is for above average rainfall in what historically is a fairly important window for crop development. This outlook is somewhat supported by the NOAA rising prospects of La Nina thresholds being reached in 4QCY25. Recent SHV announcements pointed to a strong pollination across the SA orchards.

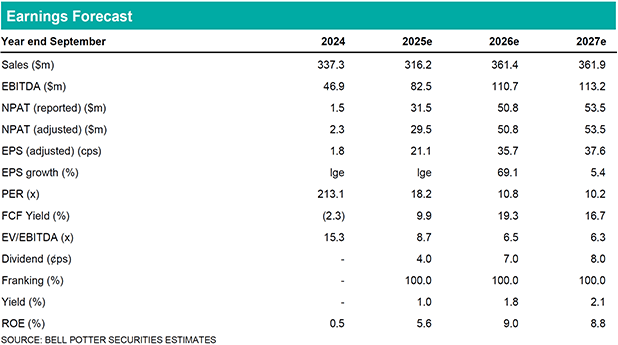

YTD VWAP pricing having consideration for the SHV hedge position would imply a FY25e pricing outcome at ~A$10.15/kg, before accounting for any achieved SHV market premiums. EBITDA changes are +4% in FY25e, +53% in FY26e and +52% in FY27e. Our NPV based target price lifts to $5.45ps (prev. $5.30ps).

Investment view: Buy rating unchanged

Buy rating is unchanged. Volatility in almond pricing has been a feature since May’25. However, the long-term under development of orchards in California implies a period of limited supply expansion potential, which we view as a positive for the direction of future almond pricing trends. Trading at ~7% discount to market NAV, ~5.9x FY26e “spot price” EBITDA and ~9.3x FY26e “spot price” PER (@29kt production), valuation is undemanding, particularly if pricing continues to firm.